The California Supreme Court Case overturning the ban on same sex marriage has led some observers to argue that the repeal of the ban on same-sex marriage is the start of a slippery slope to polygamy. Recent events in the West Texas town of El Dorado uncovered a polygamous compound of the FLDS (Fundamentalist Church of Jesus Christ of Latter Day Saints). While the compound is real, polygyny is also rare in industrialized economies. A recent article in the American Economic Review by Eric Gould, Omer Moav, and Avid Simhon (vol. 98, no. 1, pp.333-357) explains why. The authors build a model that explains the transition from polygyny to monogamy. Stripped to its bare essentials, the authors repeat the biological and anthropological argument that polygyny tends to arise in economies where males have unequal endowments of wealth or earnings. Male inequality allows the richest males to attract multiple females who produce large quantities of children.

How does the transition to monogamy occur? The authors first make the case that the source of male income is itself a determinant of polygyny. When male income and wealth are derived from non-labor sources such as land and natural resources or via corruption as they frequently are in less developed economies, rich males have a comparative advantage in producing large quantities of children. As industrialization proceeds, the return to land and natural resources declines and the returns to human capital rise. A key characteristic of the development process is that women are allowed to become more productive. As female inequality in human capital increases, males and females with high levels of human capital begin to enjoy a comparative advantage in producing quality (educated) children. In addition, as female inequality in human capital increases, women gain the upper hand in determining the terms of the marriage contract and are able to extract (enforce) a monogamous, rather than polygynous contract, from males.

My interpretation of the author's model is that the slippery slope argument against same-sex marriage is a straw man, unlikely to lead the way to polygamous marriage in the future.

Tuesday, May 27, 2008

Tuesday, April 22, 2008

Unintended consequences of the death penalty for child rapists

The Southeast Missourian newspaper reports that Governor Matt Blunt would like to extend the death penalty for child rapists. While child rape is a heinous crime, increasing the penalty might actually cause an increase in murders of children who have been raped. Economist Don Boudreaux argues that once a rapist commits the rape and they are subject to being executed if caught, the rapist has the incentive to get rid of the eyewitness. "Punishing rape less severely than murder ensures that rapists still have something more to lose if they kill their victims."

Thursday, April 10, 2008

Wednesday, April 2, 2008

Food for Thought

This from Holman Jenkins in today's WSJ: "Of the nation's $11 trillion in housing debt, at most about $1 trillion is 'unfunded.' How much more likely is the political class to fail us when confronting $99 trillion in unfunded entitlement liability?"

Thursday, March 27, 2008

Words of Wisdom

This from Allan Meltzer in today's WSJ,

"If the government underwrites all the risks, call it socialism. If it underwrites only the failures, call it foolishness."

"If the government underwrites all the risks, call it socialism. If it underwrites only the failures, call it foolishness."

Monday, March 24, 2008

Behavioral Economics for Business People

Economists argue that opportunity costs are the relevant metric when it comes to making decisions. However, individuals sometime appear to weigh money costs and implicit opportunity costs differently. The result is often characterized as "loss aversion," where the disutility of giving up an object is greater than the utility associated with acquiring it. For instance,

people are often reluctant to sell a stock that has performed poorly until it is back to the price it was originally bought at. A consequence of loss aversion is that these same people become risk averse for gains, but risk-takers for losses.

I was reading V.S. Naipaul's A Bend in the River when I came across this passage that helps fix the idea. The narrator is in the process of buying a business from an owner wishing to sell and receives this advice from the owner of the business.

"You must always know when to pull out. A businessman isn't a mathematician. Remember that. Never become hypnotized by the beauty of numbers. A businessman is someone who buys at ten and is happy to get out at twelve. The other kind of man buys at ten, sees it rise to eighteen and does nothing. He is waiting for it to get to twenty. The beauty of numbers. When it drops to ten again he waits for it to get back to eighteen. When it drops to two he waits for it to get back to ten. Well, it gets back there. But he has wasted a quarter of his life. And all he's got out of his money is a little mathematical excitement."

people are often reluctant to sell a stock that has performed poorly until it is back to the price it was originally bought at. A consequence of loss aversion is that these same people become risk averse for gains, but risk-takers for losses.

I was reading V.S. Naipaul's A Bend in the River when I came across this passage that helps fix the idea. The narrator is in the process of buying a business from an owner wishing to sell and receives this advice from the owner of the business.

"You must always know when to pull out. A businessman isn't a mathematician. Remember that. Never become hypnotized by the beauty of numbers. A businessman is someone who buys at ten and is happy to get out at twelve. The other kind of man buys at ten, sees it rise to eighteen and does nothing. He is waiting for it to get to twenty. The beauty of numbers. When it drops to ten again he waits for it to get back to eighteen. When it drops to two he waits for it to get back to ten. Well, it gets back there. But he has wasted a quarter of his life. And all he's got out of his money is a little mathematical excitement."

Thursday, March 13, 2008

Savers of the World, Unite!

The Fed is at it again, pumping another $200 billion into the nation's supply of liquidity in an effort to undo the housing mess and credit crunch that it created. It is doubtful this will have much of an impact on the housing market except to delay the inevitable write-offs and losses that are still to come in that sector.

But it is likely that the Fed is sowing the seeds of further inflation. Pumping liquidity into the system to fix what is primarily a sector problem (excess supply and weak demand in the housing sector) never has made sense, and still doesn't. The Fed tried that in the 1970s when oil first zoomed in price and all we got was stagflation. It is beginning to look as if we may have a repeat of that era. Is it any wonder that the price of oil has gotten so high today (over $110) as the dollar has slumped to record lows?

There is no doubt that the Fed's current policies are anathema to anyone in our economy with savings. The combination of low interest rates (banks seem to be playing a game of how low can you go with the interest rates that they pay) and accelerating price increases means negative returns for anyone with money in the bank. In addition, the faltering stock market eats away at people's retirement accounts, many of whom are Baby Boomers who might like to retire soon. Where's the incentive to save in such an environment?

It might be argued that savers need to tolerate lower returns for a while for the greater good: improving the economy's performance. I could accept that argument if the Fed were actually trying to do that; but its current mix of policies seem unlikely to improve anything.

But it is likely that the Fed is sowing the seeds of further inflation. Pumping liquidity into the system to fix what is primarily a sector problem (excess supply and weak demand in the housing sector) never has made sense, and still doesn't. The Fed tried that in the 1970s when oil first zoomed in price and all we got was stagflation. It is beginning to look as if we may have a repeat of that era. Is it any wonder that the price of oil has gotten so high today (over $110) as the dollar has slumped to record lows?

There is no doubt that the Fed's current policies are anathema to anyone in our economy with savings. The combination of low interest rates (banks seem to be playing a game of how low can you go with the interest rates that they pay) and accelerating price increases means negative returns for anyone with money in the bank. In addition, the faltering stock market eats away at people's retirement accounts, many of whom are Baby Boomers who might like to retire soon. Where's the incentive to save in such an environment?

It might be argued that savers need to tolerate lower returns for a while for the greater good: improving the economy's performance. I could accept that argument if the Fed were actually trying to do that; but its current mix of policies seem unlikely to improve anything.

Wednesday, March 12, 2008

Rams for Official Missouri NFL Team!

Representative Curt Dougherty has recently proposed that Budweiser be named the official state beer of Missouri. Some citizens have scoffed at the outrageous proposal and have argued that our legislature has more important things to do. Ah, contraire. The rubbish policy proposals coming out of Jefferson City have included mandates for ethanol use and recently, another mandate for biodiesel use. Both alternative fuels cause increased CO2 emissions and require that consumers pay more at the pump. I applaud Representative Dougherty and urge other Missouri senators and representatives to come up with their own proposals for official products. I propose that debate should begin on whether the Chiefs or the Rams would be best representative of an official Missouri NFL team. The ensuing debate would take much time and keep the policy-makers from "solving" any other problems.

Monday, February 25, 2008

Two Big Numbers

Consider the following numbers: $300 billion and $700 billion. Those are the approximate sizes of the US federal government budget deficit and the US annual trade deficit with the rest of the world, respectively. The total is $1 trillion annually, a number that represents approximately the amount that the US must borrow each year from the rest of the world to finance our deficits.

To say that the US is spending more than it produces is to state the obvious. To say that the US needs to reign in its spending and increase its savings is also to state the obvious. Yet, a look at current monetary and fiscal policies makes one wonder what the government and the Fed are thinking. The Fed is feverishly lowering interest rates to stimulate spending while the Federal Government has already passed a tax rebate to help people spend more as spring approaches. Of course, the reason for these moves is to presumably forestall a recession or help us to get out of one that we may already be in.

Given that consumers will not get checks until May and given that Fed policy takes 6-8 months to have any real effect, the question has to be: why are we doing this? Why is the Federal Government spending money it doesn't have and why is the Fed lowering interest rates only to set us up for the next bubble that it will create (recall the tech stock boom of the late 1990s and the housing boom most recently-both Fed caused)? The recession/slow growth will end by June/July at the latest and the economy will start to recover, regardless of the stimulus packages that the government and the Fed have concocted. Are we going back to the days of stop/start economic policies that we experienced in the 1970s/1980s? We can hope we are not, but it is beginning to look as if this is the case.

To say that the US is spending more than it produces is to state the obvious. To say that the US needs to reign in its spending and increase its savings is also to state the obvious. Yet, a look at current monetary and fiscal policies makes one wonder what the government and the Fed are thinking. The Fed is feverishly lowering interest rates to stimulate spending while the Federal Government has already passed a tax rebate to help people spend more as spring approaches. Of course, the reason for these moves is to presumably forestall a recession or help us to get out of one that we may already be in.

Given that consumers will not get checks until May and given that Fed policy takes 6-8 months to have any real effect, the question has to be: why are we doing this? Why is the Federal Government spending money it doesn't have and why is the Fed lowering interest rates only to set us up for the next bubble that it will create (recall the tech stock boom of the late 1990s and the housing boom most recently-both Fed caused)? The recession/slow growth will end by June/July at the latest and the economy will start to recover, regardless of the stimulus packages that the government and the Fed have concocted. Are we going back to the days of stop/start economic policies that we experienced in the 1970s/1980s? We can hope we are not, but it is beginning to look as if this is the case.

Wednesday, February 20, 2008

Possible Causes of the Industrial Revolution

I've just finished reading Greg Clark's book, A Farewell to Alms, available in Kent Library. Clark addresses a few very interesting questions. First, why did the Industrial Revolution begin in England and not Japan or China or India or somewhere else? Second, why did the great expansion in economic well-being begin around 1780 and not before? Third, what were the drivers behind the escape from the Malthusian trap where, for thousands of years, advances in technology resulted in short-term per capita income gains which were wiped out by an expansion in the population?

Clark examines the main economic growth theories and finds them all insufficient as explanations for growth. Instead, Clark argues that there were four main drivers of the Industrial Revolution that occurred over centuries. First, interest rates declined because individuals became more patient and willing to defer gratification. In an interesting section, Clark gives evidence that forager/hunter societies have very high rates of time preference (they strongly prefer current consumption to future consumption). For example, the Yanomamo of Brazil, have such a high rate of time preference that they cut the branches off berry bushes to make picking easier, even though it reduces future harvests and even kills the bush. The decline in interest rates allowed greater accumulation of capital which helped fuel growth. Second, economic growth occurred because of greater willingness to work more. People in forager societies lived at the subsistence level but worked little; on average the male Yanomamo worked between three and six hours a day, while male laborers in England worked between eight and nine hours per day, but also existed at the subsistence level. However, the longer work hours became a cultural norm and helped enhance efficiency as the world went through the demographic transition to lower population growth. Third, "literacy and numeracy went from a rarity to the norm." Numeric skills were needed to facilitate the use of money as a medium of exchange, rather than barter, and ultimately allowed technological innovation to spread. Finally, there was a decline in interpersonal violence. While Clark glosses over this driver of growth, I would argue that the decline in interpersonal violence gave rise to greater trust between individuals. Without trust, voluntary trade between strangers is more difficult resulting in a loss of the gains from specialization according to comparative advantage.

Clark provides evidence on a wide range of economic and social indicators between various hunter/gatherer societies and more industrial societies to build his case. He looks at height, fertility rates, calorie consumption, work hours, transportation costs, population, profit rates, interest rates, land rents, and wages. Clark's overall theme seems to suggest that the industrial revolution occurred in England and Europe because of cultural changes, rather than institutional changes, such as greater reliance on private property rights and markets and limited government.

Clark examines the main economic growth theories and finds them all insufficient as explanations for growth. Instead, Clark argues that there were four main drivers of the Industrial Revolution that occurred over centuries. First, interest rates declined because individuals became more patient and willing to defer gratification. In an interesting section, Clark gives evidence that forager/hunter societies have very high rates of time preference (they strongly prefer current consumption to future consumption). For example, the Yanomamo of Brazil, have such a high rate of time preference that they cut the branches off berry bushes to make picking easier, even though it reduces future harvests and even kills the bush. The decline in interest rates allowed greater accumulation of capital which helped fuel growth. Second, economic growth occurred because of greater willingness to work more. People in forager societies lived at the subsistence level but worked little; on average the male Yanomamo worked between three and six hours a day, while male laborers in England worked between eight and nine hours per day, but also existed at the subsistence level. However, the longer work hours became a cultural norm and helped enhance efficiency as the world went through the demographic transition to lower population growth. Third, "literacy and numeracy went from a rarity to the norm." Numeric skills were needed to facilitate the use of money as a medium of exchange, rather than barter, and ultimately allowed technological innovation to spread. Finally, there was a decline in interpersonal violence. While Clark glosses over this driver of growth, I would argue that the decline in interpersonal violence gave rise to greater trust between individuals. Without trust, voluntary trade between strangers is more difficult resulting in a loss of the gains from specialization according to comparative advantage.

Clark provides evidence on a wide range of economic and social indicators between various hunter/gatherer societies and more industrial societies to build his case. He looks at height, fertility rates, calorie consumption, work hours, transportation costs, population, profit rates, interest rates, land rents, and wages. Clark's overall theme seems to suggest that the industrial revolution occurred in England and Europe because of cultural changes, rather than institutional changes, such as greater reliance on private property rights and markets and limited government.

Friday, February 8, 2008

Presidents, Economic Growth, and CO2 Emissions' Growth

Since 1960, Democratic presidents have achieved higher average annual rates of real GDP growth than Republic Presidents. As concern about global warming mounts among scientists, policy-makers, and citizens, how do the different presidents fare on CO2 emissions? Reading from left to right we have Bush II, Bush I, Nixon/Ford, Carter, Reagan, Clinton, and JFK/LBJ. Higher growth rates of real GDP per capita are strongly correlated (r=0.72) with higher growth rates of emissions. Of course, correlation does not prove causation, but it should give pause for concern about the difficult tradeoffs society faces concerning future emissions and economic growth.

The Barbarian Invasions

For foreign film aficionados, The Barbarian Invasions is good pick, as a dying French Canadian university professor is tended to by his economist/financier son. In addition to a great story, the film causes the viewer to look closely at Canada's health care system and the role of markets in bringing together the "sensual socialist" professor and his "puritanical capitalist" son. In Kent Library, IM DV 479.

Tuesday, February 5, 2008

Pretense of Knowledge in Financial Economics

A colleague called me to task for my criticism of constructivist macroeconomists at the Federal Reserve and macroeconomists in general for their persistent support of discretionary stabilization policy despite evidence indicating such policies are pro-cyclical. What Hayek called a “pretense of knowledge” and a reliance on artificial mathematical precision is also apparent among financial economists. Taleb, author of the Black Swan, argued that the pretense of understanding was even worse among financial economists. Economists are more often content to predict the direction of change while much of the financial economics, including the theory of asset and derivative pricing, presumes to predict magnitudes. Despite a preponderance of evidence indicating stock returns are non-normal much of finance theory assumes normality in returns with constant conditional variance. Accordingly, under the assumptions of a normal distribution stock market declines such as the ones in 1987 and 1997 are only supposed to happen every 500 years.

The over reliance on artificial mathematical precision may also be more apparent in financial economics. Over the last decade many Wall Street investment banking firms relied on PhDs in statistical physics to quantify risk in securitized lending such as the sub-prime secondary market despite their having little institutional understanding of how these markets operate. Clearly, many of the models perpetuated by Wall Street were wrong but you can afford to be wrong if you can rely on the Bernanke put.

The over reliance on artificial mathematical precision may also be more apparent in financial economics. Over the last decade many Wall Street investment banking firms relied on PhDs in statistical physics to quantify risk in securitized lending such as the sub-prime secondary market despite their having little institutional understanding of how these markets operate. Clearly, many of the models perpetuated by Wall Street were wrong but you can afford to be wrong if you can rely on the Bernanke put.

Thursday, January 31, 2008

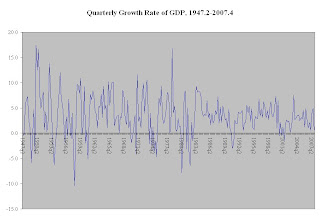

Decline in GDP Volatility

Although the Fed has not targeted money aggregates for some time, several explanations have been offered for the decline in the volatility of GDP since the early 1980s. These include financial deregulation/innovation, improvements in supply chain management that have substantially reduced inventory backlogs associated with economic down turns, inflation booms that have been tempered by global competition and the absence of major macroeconomic shocks like an OPEC oil embargo. Although greater Fed transparency, beginning with the publication of Federal Open Market Committee meeting minutes in 1994 reduced uncertainty regarding Fed policy, this has had more of an impact on volatility in financial markets rather than volatility in the real economy.

FED Policy has reduced GDP volatility

In the late 1970s the Federal Reserve, under Paul Volcker, effectively abandoned interest rate targets and instead began targeting the money supply. While Fed economists and policy-makers might sometimes advocate "fine-tuning" and discretionary policy, the proof is in the pudding as the volatility in GDP growth has declined considerably since the 1980s. Milton Friedman argued that the test of a good model is its ability to predict. On that basis, the so-called "interventionist" policies seem to have worked.

Wednesday, January 30, 2008

Fed Policy and a Pretense of Knowledge

If economics is “real science” a notion that Nassim Taleb bestselling author of the Black Swan disputes, then one might expect some consistency among economic scientists in regard to fundamental principle. The fundamental principle of capitalism is the self-correcting nature of market systems. Yet, the majority of the economics profession is not yet convinced that markets work. To me, this is analogous to saying that a majority of physicists disagree with gravity.

It is little wonder that practitioners of the dismal science have largely failed as popular champions of spontaneous order. Constructivist macroeconomists at the Federal Reserve and elsewhere continue to perpetuate the myth of discretionary fiscal and monetary stabilization policy despite an empirical record of failure documented in Friedman and Schwartz’s (1963)

Friday, January 25, 2008

Greenhouse Gas Emissions and the T3 Tax

The IPCC (Intergovernmental Panel on Climate Change) presents evidence from scientists in many fields that burning coal and oil has increased CO2 emissions by 70% from 1970 to 2004. Other emissions, including methane (CH4) and nitrous oxides (NO2), have also increased. Such GHG (greenhouse gas) emissions are thought to be a source of global warming. Adding a sense of urgency, the IPCC reports that eleven of the last twelve years have been the warmest on record since 1850, when widespread recording of temperatures began.

According to IPCC scientist and economist Ross McKitrick, "climate change models predict that, if greenhouse gases are driving climate change, there will be a unique fingerprint in the form of a strong warming trend in the tropical troposphere, the region of the atmosphere up to

Wednesday, January 23, 2008

Did the Fed Panic?

The Federal Reserve's decision to lower the Federal Funds rate on Tuesday, January 22, was a surprise on two fronts: (1) the size of the cut was the largest since at least 1990, (2) the move was made in advance of the Fed's regularly scheduled policy meeting next week. While some people are doubtless happy about the cut, others are concerned that the Fed maybe has lost control of the situation. Has the Fed panicked? That may be a little harsh, but it is clear that the Fed now realizes that the economy is in worse shape than it realized and that may be one reason why the stock market was still down on Tuesday and is down again in early trading on Wednesday.

The "r" word is getting tossed around a lot lately, but it is interesting that we do not even know yet if GDP growth has turned negative (the preliminary figures for GDP for the fourth quarter of 2007 will not be released until next Wednesday, January 30). One Federal Reserve Bank President, William Poole of the St. Louis Fed, voted against the emergency rate cut saying that he did not think conditions warranted it. I have to agree with him-to me, the Fed's move seems like it has lost control and is responding to events rather than anticipating them. And is the Fed just setting us up for the next bubble by again deciding to flood the markets with liquidity?

The "r" word is getting tossed around a lot lately, but it is interesting that we do not even know yet if GDP growth has turned negative (the preliminary figures for GDP for the fourth quarter of 2007 will not be released until next Wednesday, January 30). One Federal Reserve Bank President, William Poole of the St. Louis Fed, voted against the emergency rate cut saying that he did not think conditions warranted it. I have to agree with him-to me, the Fed's move seems like it has lost control and is responding to events rather than anticipating them. And is the Fed just setting us up for the next bubble by again deciding to flood the markets with liquidity?

Friday, January 18, 2008

Summer Opportunity for Students

The Political Economy Research Center in Bozeman, Montana offers a one week seminar for

students interested in environmental economics. The information on how to apply is here.

students interested in environmental economics. The information on how to apply is here.

Hayek and Hero Teachers

Friedrich Hayek argued that social constructs such as markets, language, the legal system, etc., were evolved processes derived from collective experience. While Hayek accepted that there were experts who harbored knowledge in specialized fields, he believed that the most important knowledge in society was widely dispersed among the population. Accordingly, no small group of central planners could ever hope to duplicate the hundreds of millions of decisions necessary to produce a top-down economic outcome superior to the one produced by a bottom-up market system.

Rather than the enlightened advice of a few elites, Hayek believed that a functioning society depended more on the distilled experience of the many which could be codified into rules of behavior. This collective knowledge is transmitted socially in largely inarticulate form leading to a “spontaneous order.” Competition among institutions results in the survival of cultural traits and behaviors that “work” even if the winners or losers never fully understand why they worked. To quote Hayek, there is “more ‘intelligence’ incorporated in the system of rules of conduct than in man’s thoughts about his surroundings.”

The inferior outcome resulting from intervention in evolved processes is not confined to market systems. For example, some educators and the media have perpetuated the myth of an idealistic hero teacher who enters an inner-city school and is shocked by the educational inadequacies. The hero teacher perseveres and by innovative teaching methods, personal sacrifice and a lot of heart inspires the students to win the state championship in music, mathematics, etc. We have all seen the movie but there is only one problem; to quote Tabarrock in Marginal Revolution “hero teachers are not replicable.” If hero teachers are required to save education then our children are in deep trouble. Fortunately, studies have shown there is a replicable method of teaching based on evolved process that does not require the instructor to be a hero. The method is known as Direct Instruction and employs a carefully constructed teaching script based on rules that rely more on perspiration than inspiration. Predictably, education elites vilify the Direct Instruction method as “rote learning” and instead advocate that every teacher blaze their own educational trail and aspire to hero status.

The myth of the hero teacher is also prevalent in higher education, particularly among universities with cultures that are still mired in their "teachers college" past. T he Direct Instruction script in higher education mean teaching a course that reflects the evolved body of knowledge within the professor's discipline. For students who want to be charmed, entertained or inspired it is cheaper to rent a movie, read a book or go to church.

Thursday, January 17, 2008

SteriodMania

The steroid controversy in baseball just is not going away. The Mitchell Report and the hearings in Congress continue to keep the problem in the public's eye. The use of steroids appears to have been fairly widespread in baseball before the advent of random testing last year. As with any activity, there are winners and losers. The winners, of course, are those who took steroids and other performance-enhancing drugs to improve and prolong their careers. Given the millions of dollars involved if one can prolong his career and/or enhance performance, it is not particularly surprising that an athlete would choose to use illegal drugs.

One columnist, Mike Celzic, indicates that the true losers are the minor leaguers who never made it to the majors because of the use of illegal drugs by major league baseball players. Celzic reports of at least one minor leaguer (Rich Harman) who is contemplating a suit against major league baseball claiming that its failure to stem the usage of performance-enhancing drugs led to he and many other minor leaguers having their paths to the big leagues blocked, presumably because many players who might otherwise have retired or would not have been successful in the big leagues without the illegal drugs were able to stay on.

This is probably a long shot of a lawsuit and legal scholars are divided on whether such a suit would have merit in a court of law. The claimant would have a pretty huge burden of proof to show that he was harmed. But the efficiency aspects of it are intriguing. If baseball players who used performance-enhancing drugs could be sued by minor leaguers claiming that their path to the big leagues was blocked by such cheats, this might be a more effective way to lead to the desired result, which, of course, is not to use the drugs. One successful suit for millions of dollars in damages might be enough to give correct incentives to all big league players to stay clean.

One columnist, Mike Celzic, indicates that the true losers are the minor leaguers who never made it to the majors because of the use of illegal drugs by major league baseball players. Celzic reports of at least one minor leaguer (Rich Harman) who is contemplating a suit against major league baseball claiming that its failure to stem the usage of performance-enhancing drugs led to he and many other minor leaguers having their paths to the big leagues blocked, presumably because many players who might otherwise have retired or would not have been successful in the big leagues without the illegal drugs were able to stay on.

This is probably a long shot of a lawsuit and legal scholars are divided on whether such a suit would have merit in a court of law. The claimant would have a pretty huge burden of proof to show that he was harmed. But the efficiency aspects of it are intriguing. If baseball players who used performance-enhancing drugs could be sued by minor leaguers claiming that their path to the big leagues was blocked by such cheats, this might be a more effective way to lead to the desired result, which, of course, is not to use the drugs. One successful suit for millions of dollars in damages might be enough to give correct incentives to all big league players to stay clean.

Wednesday, January 16, 2008

Schwarz is critical of FED

Anna Schwarz, co-author with Milton Friedman of A Monetary History of the United States, 1867-1960 is critical of current Fed chairman Ben Bernanke. Hat tip: Alex Tabbarok of Marginal Revolution. Since 1980 the monetarist regimes of the Fed have been largely successful at controlling inflation, but easy credit conditions following the bursting of the tech stock bubble in 2000 probably contributed to the sub-prime mortgage crisis.

Welcome

We welcome all visitors to our blog. Please feel free to respond to the posts made by our faculty. We look forward to a lively, interesting discussion of current events and issues in economics and finance.

Subscribe to:

Posts (Atom)

{kind=link}